DMS Strategy & Model Portfolio Leverage

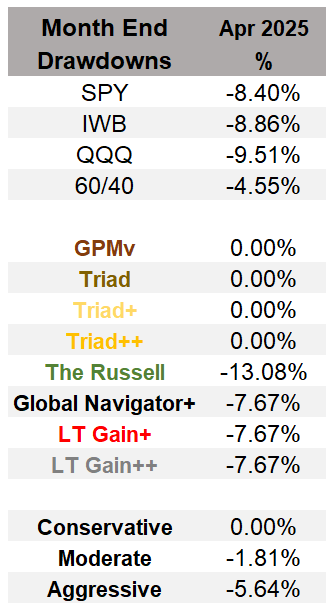

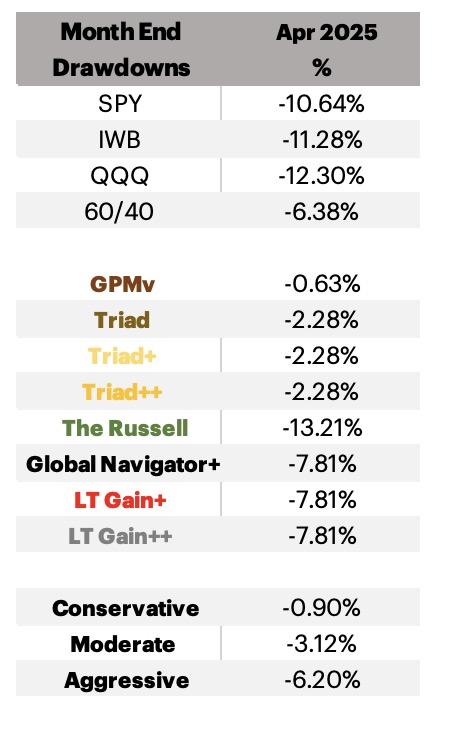

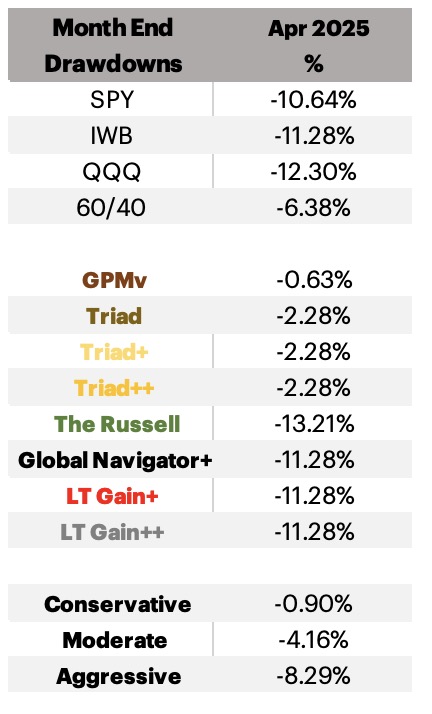

Leverage has been on my mind of late. When I re-worked the DMS Strategies for RIA purposes, it surprised me at how low the max drawdown was for even the Ultra Aggressive Model Portfolio. Judging by MaxDD alone, I don’t think anybody can fault even my most aggressive strategy because it is currently under 14% from 1980 to date. This is 42% less MaxDD than the 60/40 with over double the returns.

Why not throw caution to the wind, shouldn’t I suggest this Ultra Aggressive Model Portfolio would suit everybody? I would not, because of the high amount of leverage that the portfolio at times uses. Even though the portfolio has not seen large drawdowns to date, that doesn’t mean that they may not happen in the future. I will paraphrase Meb Faber ‘Your largest drawdown is still to come.’

GPMv: 100% is the max position, no leverage

Triad: 100% is the max position, no leverage

Triad+: 135% maximum leverage

Triad++: 170% maximum leverage

Global Navigator+: 200% maximum leverage

Global Navigator++: 300% maximum leverage

LT Gain+: 200% maximum leverage

LT Gain++: 300% maximum leverage

I would think it far too risky to put a large chunk of a person’s investments into a single strategy with a lot of leverage. LT Gain++ has the biggest drawdown of all the strategies, 28.47%. Not diversified enough, highly concentrated, higher potential for a large draw down.

Here are the maximum positions of the RIA versions of the Model Portfolios:

Model Ultra Conservative: 100% is the max position, no leverage.

Model Conservative: 125% maximum leverage

Model Moderate: 149% maximum leverage

Model Aggressive: 194% maximum leverage

Model Ultra Aggressive: 216% maximum leverage

As I thought about these maximum leverage positions in the Model Portfolios, it didn’t sit right with me, the reason is that these are more diversified than the dual momentum strategies which are often in 100% equity position and sometimes leveraging that full position. The Model Portfolios are constructed to have a more diverse allocation and from different strategies to reduce volatility and maximum drawdowns. I eventually came to think of the holdings in the Model Portfolios as belonging to one of two categories: Equities or Alternatives.

Since the Alternatives (consisting of ETF’s of things like Gold, Commodities, Managed Futures, Treasuries, Real Estate, etc.) are generally not strongly correlated to Equities as a whole, I decided that from my perspective, I want to see the maximum leverage position of the Model Portfolios in Equities only, not including the Alternatives. This is a better alignment with my risk outlook.

Here are the maximum positions and the maximum equity positions of the RIA versions of the Model Portfolios:

Model Ultra Conservative: No leverage used, 54% is the maximum equity position

Model Conservative: 125% maximum leverage, 94% maximum equity position

Model Moderate: 149% maximum leverage, 118% maximum equity position

Model Aggressive: 194% maximum leverage, 166% maximum equity position

Model Ultra Aggressive: 216% maximum leverage, 186% maximum equity position

Some of the RIA version strategies/allocations:

Triad+: 135% maximum leverage, 105% maximum equity position

Triad++: 170% maximum leverage, 140% maximum equity position

Global Nav+ & LT Gain+: 200% maximum leverage and 200% maximum equity position

Global Nav++ & LT Gain++: 300% maximum leverage and 300% maximum equity position

Bamboo+ Allocation: 123% maximum leverage, 68% maximum equity position

Bamboo++ Allocation: 204% maximum leverage, 102% maximum equity position

From my perspective, I would look at Bamboo++ with 102% maximum equity position as FAR less risky than say Global Navigator++ with 200% maximum equity. Both have “++” in the name, and both use 3X S&P leveraged ETF’s, but Bamboo only does it on roughly 1/3rd of the portfolio, while GN+ does it on 100% of the portfolio.

We’ve always had the MaxDD to evaluate for riskiness, as well as the Ulcer Index (the higher the Ulcer Index the more volatility.) I am not a person who gambles and goes with maximum position for highest expected returns. I want to generate great returns with low risk, low MaxDD, low Ulcer Index, aka Risk Adjusted returns. The Ulcer Performance Index and the Gain to Pain figures on the Metrics charts do just this, they show how good the returns are for the risk taken.

If you have any questions or comments on this please reach out.

Until I decide whether to go the RIA route or not, I am offering the RIA strategies on a $100/6 month or $200/12 month subscription basis. There has been good interest so far, I can say I think the cost for this is a steal.

Why not throw caution to the wind, shouldn’t I suggest this Ultra Aggressive Model Portfolio would suit everybody? I would not, because of the high amount of leverage that the portfolio at times uses. Even though the portfolio has not seen large drawdowns to date, that doesn’t mean that they may not happen in the future. I will paraphrase Meb Faber ‘Your largest drawdown is still to come.’

GPMv: 100% is the max position, no leverage

Triad: 100% is the max position, no leverage

Triad+: 135% maximum leverage

Triad++: 170% maximum leverage

Global Navigator+: 200% maximum leverage

Global Navigator++: 300% maximum leverage

LT Gain+: 200% maximum leverage

LT Gain++: 300% maximum leverage

I would think it far too risky to put a large chunk of a person’s investments into a single strategy with a lot of leverage. LT Gain++ has the biggest drawdown of all the strategies, 28.47%. Not diversified enough, highly concentrated, higher potential for a large draw down.

Here are the maximum positions of the RIA versions of the Model Portfolios:

Model Ultra Conservative: 100% is the max position, no leverage.

Model Conservative: 125% maximum leverage

Model Moderate: 149% maximum leverage

Model Aggressive: 194% maximum leverage

Model Ultra Aggressive: 216% maximum leverage

As I thought about these maximum leverage positions in the Model Portfolios, it didn’t sit right with me, the reason is that these are more diversified than the dual momentum strategies which are often in 100% equity position and sometimes leveraging that full position. The Model Portfolios are constructed to have a more diverse allocation and from different strategies to reduce volatility and maximum drawdowns. I eventually came to think of the holdings in the Model Portfolios as belonging to one of two categories: Equities or Alternatives.

Since the Alternatives (consisting of ETF’s of things like Gold, Commodities, Managed Futures, Treasuries, Real Estate, etc.) are generally not strongly correlated to Equities as a whole, I decided that from my perspective, I want to see the maximum leverage position of the Model Portfolios in Equities only, not including the Alternatives. This is a better alignment with my risk outlook.

Here are the maximum positions and the maximum equity positions of the RIA versions of the Model Portfolios:

Model Ultra Conservative: No leverage used, 54% is the maximum equity position

Model Conservative: 125% maximum leverage, 94% maximum equity position

Model Moderate: 149% maximum leverage, 118% maximum equity position

Model Aggressive: 194% maximum leverage, 166% maximum equity position

Model Ultra Aggressive: 216% maximum leverage, 186% maximum equity position

Some of the RIA version strategies/allocations:

Triad+: 135% maximum leverage, 105% maximum equity position

Triad++: 170% maximum leverage, 140% maximum equity position

Global Nav+ & LT Gain+: 200% maximum leverage and 200% maximum equity position

Global Nav++ & LT Gain++: 300% maximum leverage and 300% maximum equity position

Bamboo+ Allocation: 123% maximum leverage, 68% maximum equity position

Bamboo++ Allocation: 204% maximum leverage, 102% maximum equity position

From my perspective, I would look at Bamboo++ with 102% maximum equity position as FAR less risky than say Global Navigator++ with 200% maximum equity. Both have “++” in the name, and both use 3X S&P leveraged ETF’s, but Bamboo only does it on roughly 1/3rd of the portfolio, while GN+ does it on 100% of the portfolio.

We’ve always had the MaxDD to evaluate for riskiness, as well as the Ulcer Index (the higher the Ulcer Index the more volatility.) I am not a person who gambles and goes with maximum position for highest expected returns. I want to generate great returns with low risk, low MaxDD, low Ulcer Index, aka Risk Adjusted returns. The Ulcer Performance Index and the Gain to Pain figures on the Metrics charts do just this, they show how good the returns are for the risk taken.

If you have any questions or comments on this please reach out.

Until I decide whether to go the RIA route or not, I am offering the RIA strategies on a $100/6 month or $200/12 month subscription basis. There has been good interest so far, I can say I think the cost for this is a steal.